RINs break $2 as US biofuels market detaches

- Henri Bardon

- 3 minutes ago

- 3 min read

With most of Europe and Asia closed for May Day, price discovery today sat almost entirely in the US. Liquidity was thin and participation limited, which tends to amplify moves, but the direction was clear and internally driven.

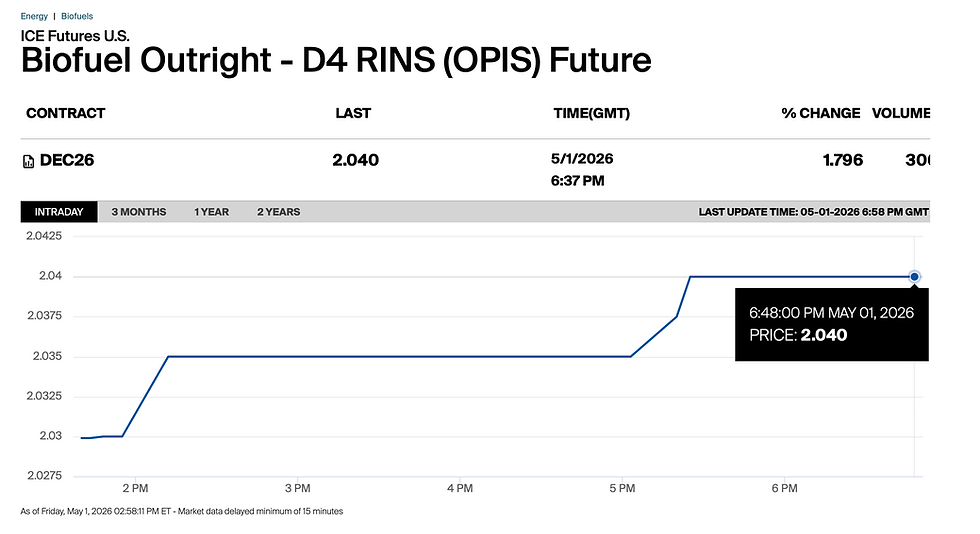

The dominant move sits in US credits. D4 RINs have pushed clearly above $2 per gallon, with Dec trading at 2.04. This is a clean break. The market is no longer pricing balance, it is pricing shortage. At these levels, RINs are rationing demand and forcing supply to respond. Politically these RINs level will start causing an uproar with refiners - something the market is not pricing.

Distillates continue to anchor the system. Heating oil remains near 4.00 $/gal on the front despite a pullback, and cracks are still elevated on a historical basis. Crude weakened, with WTI at 102 and Brent near 114, but the constraint is not crude. The constraint is clean products. Diesel and jet tightness keeps biodiesel and renewable diesel embedded in the pool.

Margins show the stress once you move away from prompt. RD screen crush for May is still positive near 0.30 $/gal, but June drops toward 0.08 and the curve turns negative into Q4. Conventional biodiesel holds better but still compresses from about 0.86 in May to the low 0.40s by year end. The forward curve does not clear without either higher RINs or lower feedstocks.

EIA data released today adds an important layer. Total feedstock use for February increased by 12.41 percent year on year versus February last year. The ramp is still gradual, but the composition is shifting fast. Soybean oil moved from 28 percent to 44 percent of the mix, canola doubled from 4 percent to 8 percent, and corn oil held at 14 percent. At the same time, tallow dropped from 30 percent to 21 percent and yellow grease from 22 percent to 11 percent. White grease remained marginal at 2 percent. This is a clear move back into vegetable oils, consistent with winter specifications where cold flow properties matter and limit the use of animal fats.

Bean oil confirms the US isolation. Prices are back near 1,690 $/mt, with the bean oil to gasoil ratio at 1.31 for May. This sits well above global comparables. Outside the US, soft oils remain cheaper, but the RFS structure keeps domestic pricing elevated. The market is pulling value into the US through RINs rather than through physical arbitrage.

BOHO reinforces the signal. The spread moved above 1.60 on the front, up more than 5 percent on the day. Heating oil continues to support blending economics, but forward structure remains weak, which explains the rapid deterioration in crush margins beyond prompt.

The Iran situation remains the anchor in the background. Roughly 20 percent of global oil and gas flows are still disrupted through the Strait of Hormuz, and negotiations are only at an early stage with no defined timeline. That keeps a structural bid under distillates even on days when crude corrects.

The conclusion is direct. RINs above $2 are now the clearing mechanism. If they hold or move higher, they will pull in imports and keep biodiesel and RD running despite weak forward margins. If they fail, the adjustment will come through lower feedstock prices or reduced run rates. Right now, credits are in control.

Comments