Hormuz Disruption Priced In as Distillate Structure Signals Stress While BOGO Collapses Nearly 10 Percent

- Henri Bardon

- 14 hours ago

- 4 min read

Energy markets opened higher on confirmation of the U.S. move to restrict Iranian shipping but failed to extend gains, with Brent trading between $98 and $102 per barrel after earlier highs above $102. This still represents a move of more than 40 percent since the initial disruption of flows through the Strait of Hormuz. The lack of follow-through reflects that a large portion of the geopolitical risk was already priced ahead of the weekend.

There are also increasing reports of heightened Iranian maritime pressure in the Gulf, including the risk of selective interdiction of vessels linked to countries aligned with the U.S. While a full counter-blockade has not been formally confirmed, even the threat of disruption across the Strait of Hormuz is enough to materially impact flows. The Strait normally handles close to 20 million barrels per day, and any restriction increases freight costs, insurance premiums, and delays, reinforcing the tightness already visible in prompt distillate markets.

The key signal remains distillates. ICE gasoil front month is trading at $1,164 per metric ton while December is near $856, leaving the May to December backwardation at +$309.50 per metric ton. The May to July spread alone is +$163.50. These levels indicate immediate diesel scarcity and force inventory liquidation across the system.

Despite this, parts of the complex moved lower. Singapore 10 ppm gasoil is down $7.45 per metric ton to $197.79 per barrel equivalent, while Fujairah gasoil is down $9.78 per metric ton. CBOT soybean oil is down 0.88 percent to 66.50 cents per pound, equivalent to $1,466 per metric ton. B100 FOB East Coast is down 2.48 percent to $6.409 per gallon. These moves reflect positioning and liquidation rather than any improvement in fundamentals.

The U.S. market continues to show strength in distillates. Heating oil is at 3.80 dollars per gallon, up 1.09 percent on the day and more than 70 percent over three months. ULSD values across key hubs range between 3.75 and 3.83 dollars per gallon. The transatlantic arbitrage remains closed, limiting Europe’s ability to attract supply.

Biofuels continue to follow distillates mechanically. D4 RINs are holding near 1.78 for December 2026. Screen biodiesel margins are now at 1.07 dollars per gallon for prompt and between 0.73 and 0.77 dollars per gallon further out the curve, up between 8 percent and 14 percent depending on tenor.

The clearest signal today is in BOGO. The spread collapsed nearly 10 percent on the day to $301 per metric ton, down from levels above $330 previously and far below recent highs above $600. On a three month basis, BOGO is now down close to 40 percent. This reflects a rapid decoupling between soybean oil and gasoil.

At current levels, gasoil is at $1,164 per metric ton while soybean oil is at $1,466 per metric ton. The ratio has compressed significantly, with bean oil now at roughly 1.25 times gasoil equivalent. Feedstocks are not tight and are not keeping pace with the distillate rally.

The broader spread complex reinforces this. BOHO is down between 6 percent and 7 percent across the curve. POGO is in clear contango with prompt at +65, July at +174, and Q4 above +280. This is a forward supply signal in feedstocks and contradicts any narrative of immediate vegetable oil scarcity.

Methanol pricing now becomes a critical constraint that the market is underestimating. Contract prices are at $1,247 per metric ton in North America and €850 per metric ton in Europe, while Asia is structurally exposed to supply disruptions given its dependence on Middle East feedstock. Methanol represents a large share of conventional biodiesel production cost, often close to 60 percent of the chemical input side of the process. At current levels, this pushes total transformation costs toward $175 per metric ton.

This effectively breaks the biodiesel substitution argument in Asia. Even if flat price diesel is high, the combination of elevated methanol costs and POGO contango means forward biodiesel production is not economically attractive. Producers are not locking in margin, they are locking in cost pressure. This is why feedstocks are not tightening despite strong diesel.

Currency markets confirm the localized nature of the move. The dollar index is down 0.25 percent to 98.20. In a typical geopolitical escalation, the dollar would strengthen. Its weakness shows that this is not a macro risk event but a physical dislocation in energy markets.

Inventory data supports the same conclusion. Global observable inventories are trending lower, with recent monthly draws exceeding 100 million barrels, driven by declines in oil in transit and floating storage. The system entered this disruption already tight, which explains the extreme backwardation.

The conclusion is clear. The market has priced the disruption into structure. Backwardation at +309 is forcing supply into the prompt market. The nearly 10 percent collapse in BOGO and elevated methanol costs confirm that feedstocks are lagging and that the stress is concentrated in distillates.

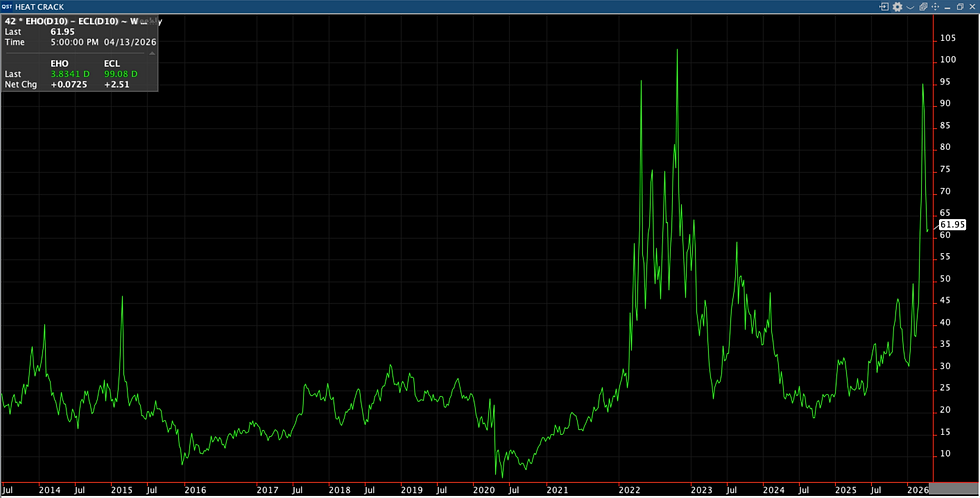

If the disruption persists, the next move higher will come from physical shortages and further widening in front spreads, not from immediate flat price strength. The Heat Crack is telling us all that we need to know trading at $61.95/Brl.

Comments