Bean Oil Indicating That a Diesel Crisis Is Straight Ahead

- Henri Bardon

- 3 minutes ago

- 3 min read

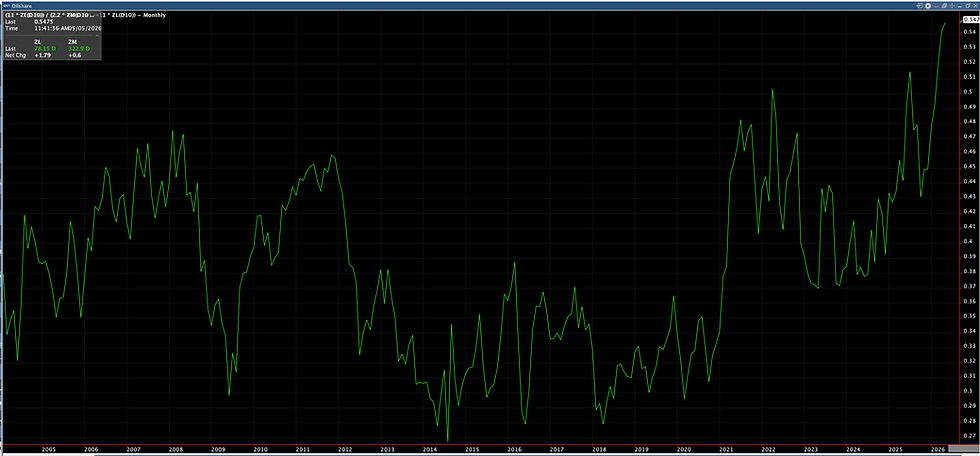

Bean oil has decisively taken control of the complex and is now trading as a forward indicator of diesel scarcity rather than an agricultural input. Front month values are near $1,720/mt equivalent with June around $1,688/mt and the curve holding strong backwardation with Jun/Dec at +5.45 c/lbs. Oilshare has reached 54.7%, a level that historically signals that the soybean complex is no longer meal-driven but fully oil-led. BOGO reflects this shift with front spreads at $452/mt and extending to $538/mt in June, showing expansion driven entirely by bean oil strength while ICE gasoil weakens.

ICE gasoil itself is trading near $1,270/mt for May, down roughly $39/mt on the session, with the forward curve still backwardated but not extending. This divergence is the key signal. Feedstocks are moving higher while the barrel is softening, which is not sustainable. The market is pulling forward a diesel shortage that is not yet reflected in flat price.

POGO highlights the dislocation but needs correct interpretation. The May contract is deeply negative at -$93/mt, largely a function of prompt positioning and liquidity. June remains negative at -$18/mt, confirming near-term weakness in palm relative to gasoil, while July rebounds to +$62/mt and Q4 trades above +$150–280/mt. Palm is not collapsing structurally. It is failing to keep pace with bean oil, which is being repriced as the marginal molecule in the system.

Physical markets remain disconnected from futures. South American soyoil basis continues to collapse, now around -2.0 to -2.5 c/lbs versus CBOT, equivalent to roughly -$44 to -$55/mt. This confirms that global supply is available but cannot clear into the U.S.-driven pricing mechanism. The domestic demand pull remains dominant and continues to distort global price relationships. I calculate that you need another 1 c/lbs to clear SouthAmerican bean oil into US.

In Northwest Europe, outright flat prices reflect strong premiums over ICE gasoil. With ICE gasoil at $1,270/mt, current indications place FAME 0 around $1,430–1,450/mt, RME closer to $1,490–1,520/mt, and UCOME near $1,600–1,620/mt flat. HVO Class II is trading around $2,550–2,600/mt flat, while SAF remains above $3,000/mt. These are elevated levels, but the rate of change remains slower than in bean oil, confirming that the dislocation is centered in feedstock rather than finished fuels.

The U.S. demand side is approaching a critical threshold. Retail gasoline is averaging $5/gal and diesel near $6/gal. Historically, once diesel approaches $6.50/gal, demand destruction accelerates. The market is now within $0.50 of that level. Despite this, futures are not pricing the risk. Heating oil remains below $4.00/gal and crude has softened, with WTI near $102 and Brent near $114. The barrel is not reflecting the stress that bean oil is already discounting.

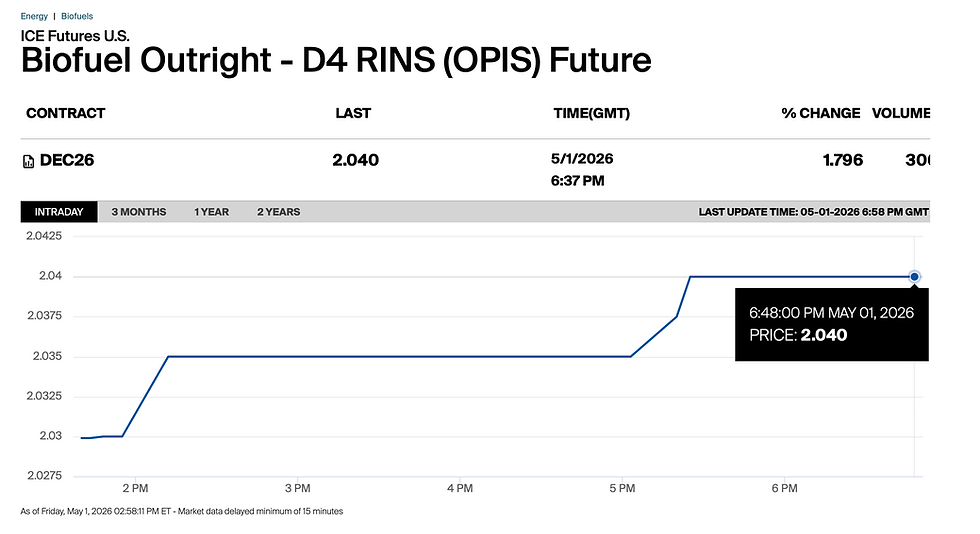

Relative value metrics reinforce the shift. Bean oil as a percentage of gasoil now stands at 1.35 in the front and extends to 1.68 further out, showing that vegetable oil is increasingly valued as a direct substitute for diesel. At the same time, biodiesel economics are deteriorating under feedstock pressure. Renewable diesel margins have effectively collapsed, with front-month crush near $0.006/gal and negative further out. Conventional biodiesel margins remain positive around $0.56/gal but are compressing steadily. D4 RINs at $2.06 for June and $2.08 for December remain elevated, yet they are not sufficient to offset the surge in feedstock costs.

Outside the U.S., the system shows early signs of demand resistance. Singapore gasoil is stable around $161.5/bbl, Fujairah near $155/bbl, and jet fuel in the $155–166/bbl range. Heat cracks remain high near $65/bbl but are not extending. In India, import margins are negative across major vegetable oils, with CPO around -$26/mt, soybean oil near -$63/mt, and sunflower oil around -$22/mt. This indicates that high prices are already curbing demand in key importing regions.

The spread between bean oil and palm oil continues to widen. CBOT bean oil is trading above $1,700/mt equivalent while CPO remains closer to $1,200–1,250/mt. This gap reflects structural demand from the U.S. rather than global tightness. Paper markets remain active, with FAME trading around $160/mt, UCOME around $345–350/mt, and HVO Q4 near $1,770–1,780/mt, but these flows reflect positioning rather than physical clearing.

The market is now split between current conditions and forward expectations. Distillates reflect present tightness but not panic. Feedstocks, led by bean oil, are pricing a serious forward shortage scenario.

Historically, bean oil leads diesel by two to three weeks in this type of environment. Oilshare at 55%, negative prompt POGO, collapsing South American basis, and retail diesel approaching $6.50/gal all point in the same direction. The system is moving toward a stress point.

Either diesel moves sharply higher to validate the signal, or demand breaks and forces a correction in feedstocks. At this stage, bean oil is leading and the rest of the barrel has yet to respond.

Comments