This Week Decides the Barrel as Distillate Tightness Meets Rising Caution

- Henri Bardon

- 1 day ago

- 5 min read

The distillate complex continues to dictate direction and the market is now at an inflection point. Singapore 10ppm gasoil is holding at $266.84 per barrel even after a sharp $21.8 per barrel daily correction, following the recent move toward $300 per barrel. The structure remains extremely tight. Naphtha cracks are now at $452 per ton over Brent with a record $143 per ton backwardation between M1 and M2, confirming severe stress across the refined barrel and feedstock chain.

The forward curve is sending an even stronger signal. ICE gasoil Apr Dec backwardation is now at plus $653.75 per ton. This is an extreme structure. It reflects a market that is aggressively pricing prompt scarcity and does not believe supply normalizes any time soon. At these levels, replacement cost dominates all pricing decisions across the barrel, including biodiesel and renewable diesel.

Saudi Arabia has moved aggressively to capture this tightness, raising May Arab Light OSPs to Asia by $17 per barrel month on month to $19.50 per barrel over Oman Dubai, with Northwest Europe pricing up to $27.85 per barrel over Brent. OSPs are the official term pricing formula Saudi uses to sell crude into each region, effectively setting the benchmark differential refiners must pay for prompt barrels. At these levels, they confirm that refiners are bidding aggressively for immediate supply. At the same time, Russian exports via Tuapse are rising to 794 thousand tons in April, but diesel flows are only up 4.2 percent, insufficient to offset the broader disruption.

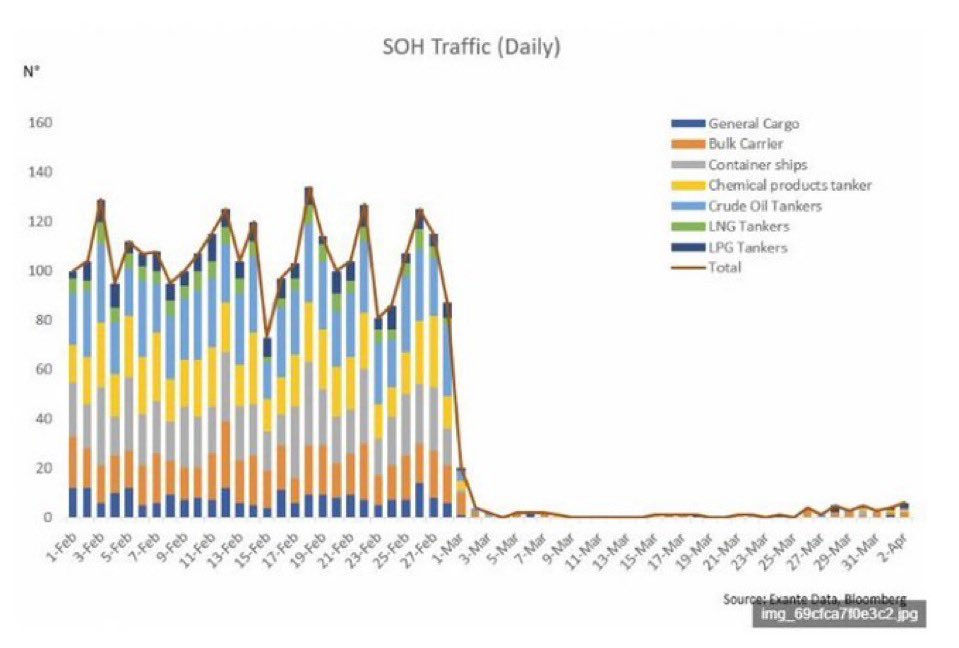

Logistics are now reinforcing the tightness. Traffic through the Strait of Hormuz has effectively collapsed, with daily vessel counts dropping from roughly 100 to 130 ships per day in February to near zero in early March, only marginally recovering into April. This is not only crude. The reduction spans refined products, chemical tankers, LNG, and LPG, confirming a system wide disruption across the entire energy complex. This is not a pricing signal, it is a physical constraint. With fewer cargoes moving across all product categories, replacement barrels take longer routes, freight costs increase, and prompt availability tightens further. This is exactly how localized disruption in East Asia transmits into global distillate scarcity.

Biofuels continue to be mechanically supported by this environment. US B100 East Coast is now $7.02 per gallon, up 4.48 percent on the day, RD California at $4.146 per gallon up 7.92 percent, HVO NWE at $3,090 per ton, and SAF NWE at $2,863 per ton. The linkage to diesel remains intact. D4 RINs at $1.80 confirm the system is still structurally short compliance, even if slightly softer intraday.

Today is also a key regulatory milestone. It is the deadline to submit comments on the proposed 45Z framework and to request participation in the May 28 hearing. This will shape how the new producer credit is implemented, including CI scoring and eligibility, and the market is clearly waiting for clarity.

However, the European paper market is sending a different signal. Over the last five weeks, volumes have been highly inconsistent. Week 9 traded above 1 million tons equivalent, followed by a collapse in week 11 and only partial recovery afterward. Week 13 shows around 670 thousand tons equivalent, still well below peak activity.

The composition also matters. Week 9 saw strong participation across all products, including roughly 427 thousand tons FAME0 and 290 thousand tons UCOME, while more recent weeks show reduced HVO and UCOME participation. This is not just lower volume, it is selective engagement.

This confirms that paper is no longer chasing the rally. Participants are stepping back, reducing exposure, and trading tactically rather than structurally. Caution is clearly back in the market.

Physical window activity reflects the same hesitation. FAME trades are still printing between minus 25 and minus 78 per ton, RME between minus 5 and minus 35 per ton, while UCOME holds a strong premium at plus 70 to plus 75 per ton and HVO Class II trades around $1,270 per ton. The spread between waste based and crop based fuels remains extremely wide.

Feedstocks continue to contradict the strength in fuels. CBOT soybean oil is now around 69.5 cents per pound, equivalent to roughly $1,534 per ton, up about 39 percent over three months. Yet BOGO continues to weaken sharply on the front to +182, with front spreads down 3 to 5 percent on the day creating a deep contango to summer months - July being at +465. This confirms that vegoil is not tightening in line with diesel.

BOPO is moving higher, up around 3 to 4 percent, reflecting soybean oil strengthening faster than palm oil. CBOT bean oil continues to push higher on flat price and relative value, while palm is rising more slowly despite supportive fundamentals. MPOB expectations still show March stocks down about 19 percent to 2.18 to 2.19 million tons, with exports up 37 to 38 percent and production only up about 4 percent. Malaysian output increased just 2.63 percent, confirming limited supply growth. Palm remains supported with FCPO at RM4,791 and resistance at RM4,800 to RM4,900, but the widening BOPO spread reflects stronger momentum in soybean oil rather than a palm led move.

Brazil is now adding another layer of complexity. Biodiesel demand is ramping up, but pricing dynamics have flipped. In many regions, biodiesel is now trading below diesel, which is incentivizing domestic consumption and pulling volumes away from export channels. Crushers are benefiting from the repricing of older contracts, while trading houses are buying back paper and redirecting soyoil into the domestic market. At the same time, Brazilian soyoil basis levels remain deeply negative, in some cases below minus 15 to minus 20 cents per pound, confirming that local supply remains abundant despite rising demand. This creates a localized surplus dynamic that stands in contrast to the global distillate tightness.

At the same time, global vegoil supply remains available. Brazilian soyoil FOB Paranagua continues to trade at deeply negative levels between minus 1000 and minus 1500 versus Chicago, confirming that physical supply is not constrained.

Geopolitics continues to distort flows. Venezuelan exports to India surged to 342 thousand barrels per day in March from 35 thousand barrels per day in February, accelerating inventory draws.

The market is now clearly bifurcated. Diesel and refined products are tight and driving flat price strength. Biofuels are supported through that linkage. But feedstocks are not tight enough to justify the move, and paper markets are stepping back.

This creates an unstable setup. If diesel pushes higher again, margins will expand quickly and pull biofuels with it. If diesel stalls or corrects, the lack of feedstock tightness and reduced paper participation will accelerate the downside.

My view is that this week is pivotal. The geopolitical path will determine direction in the very near term. If tensions escalate, diesel pushes higher and pulls the entire bio complex with it. I would expect rationing of distillate to start in East Asia and move West after the 15th, reinforcing backwardation and tightening prompt availability further. If not, the market starts pricing demand response quickly and the correction can be sharp. Today the system still trades tight, but the increase in caution across paper, spreads, and positioning is a clear warning signal.

Comments