The Peace Dividend Is Dead, Inventory Reality Is Back And Biofuels Follow Energy Higher

- Henri Bardon

- 6 hours ago

- 3 min read

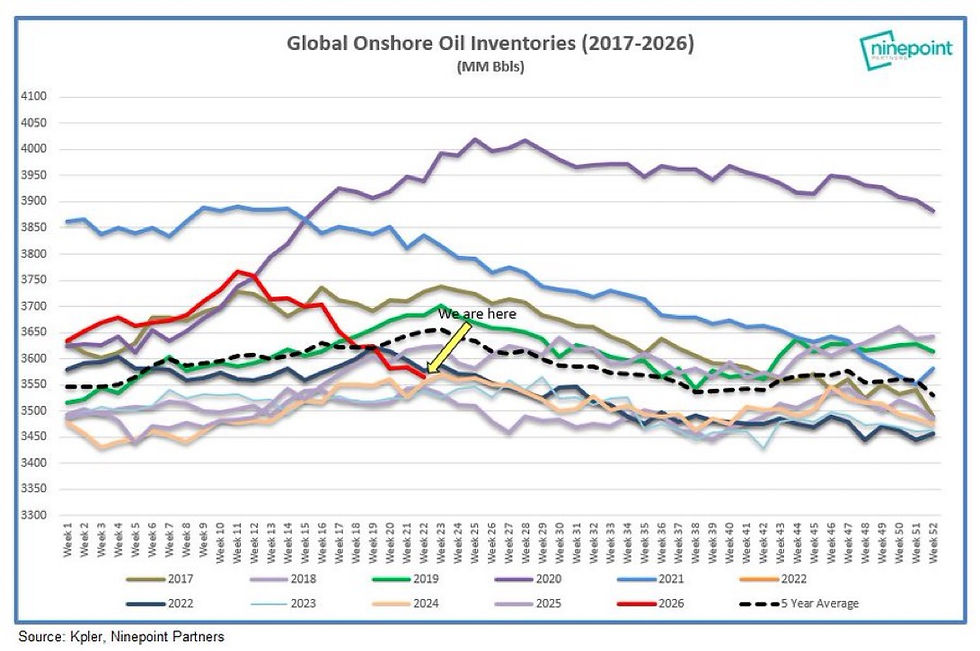

Monday's market action delivered a clear message: traders are increasingly rejecting the peace dividend narrative. Despite continuing headlines around diplomacy, crude oil rallied sharply with WTI closing above $92/bbl while soybean oil remained resilient and D4 RINs continued their advance. The reason is becoming increasingly obvious. Inventories continue moving lower almost everywhere. U.S. commercial crude inventories have fallen from roughly 465 million barrels in April to near 435 million barrels today. Global onshore inventories continue tracking below historical averages. U.S. drilled-but-uncompleted wells have fallen to just 4,972, the lowest level recorded under the current methodology, while Permian DUC inventories have dropped 36% year-on-year to only 793 wells. The industry continues drawing inventories rather than building future production capacity. At the same time, the Strategic Petroleum Reserve is now within days of falling to its lowest level since August 1983, a level not seen since the early years of the reserve's creation. We are in week 22... 8 weeks to zero hour.

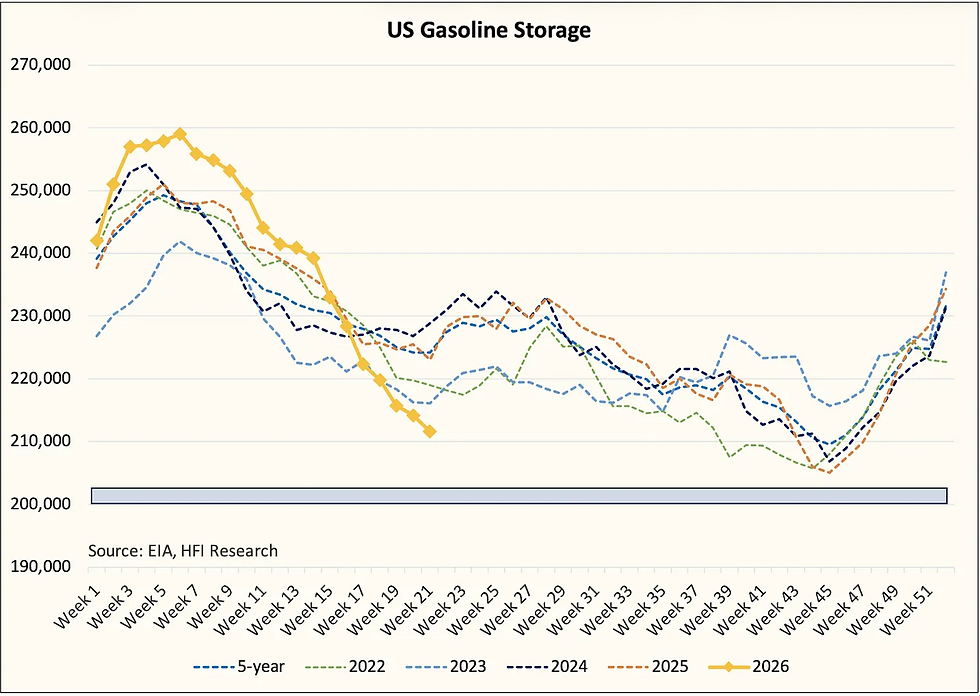

The refined products story is even more important. U.S. gasoline inventories have collapsed from nearly 260 million barrels at the beginning of the year to approximately 211 million barrels today. Distillate inventories have fallen from 133 million barrels to just above 100 million barrels, placing them roughly 15 million barrels below the five-year average. Reuters highlighted that U.S. gasoline prices have already surged following one of the longest stretches of inventory draws in recent years. You better fill up early this week in the US.

Yet the screen heat crack remains near $61/bbl, showing little sign of rationing demand. In other words, inventories are tightening while margins remain exceptionally profitable. As summer driving demand accelerates, the probability of a significant move higher in pump prices continues to increase. For biodiesel and renewable diesel traders, this matters because renewable fuels are now an integral component of the distillate pool. A stronger diesel complex ultimately supports biodiesel and renewable diesel values.

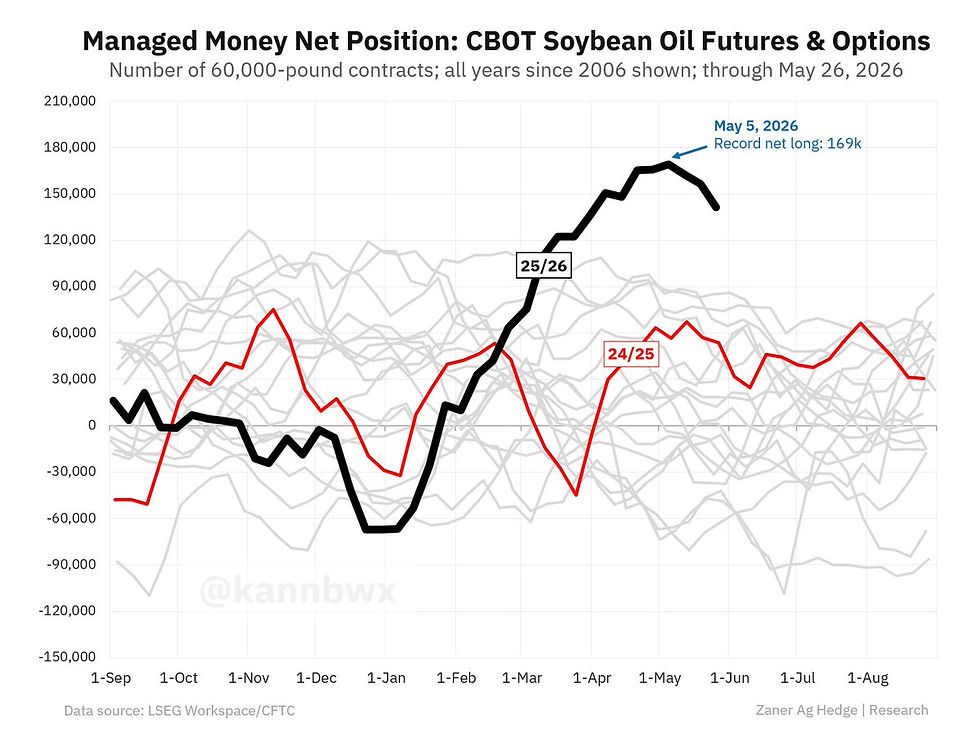

The U.S. biofuels story continues to tighten. Managed money remains historically long soybean oil, still holding roughly 140,000 contracts after reaching a record 169,000 contracts in early May. Many analysts have argued this positioning creates downside risk, yet soybean oil continues to decouple from broader energy weakness. Export inspections reached 494,000 metric tons last week, with 42% of shipments destined for China. While cumulative soybean exports remain down 20% year-on-year at 35.6 million metric tons, Chinese demand remains visible despite trade tensions.

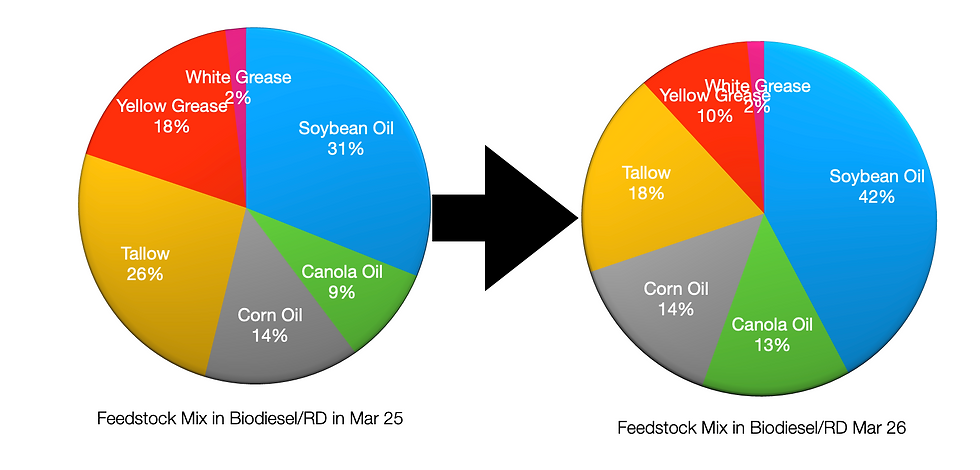

Recent EIA feedstock data reinforces why soybean oil continues to outperform. Total biodiesel and renewable diesel feedstock consumption reached 3.039 billion pounds in March, up 11.4% from 2.693 billion pounds a year earlier and up 27.4% from February's 2.386 billion pounds. More importantly, soybean oil's share of the feedstock slate surged to 42% from 31% a year ago while tallow fell to 18% from 26% and yellow grease dropped to 10% from 18%. The renewable fuels industry is becoming increasingly dependent on vegetable oils rather than waste fats, a structural shift that helps explain soybean oil's resilience.

The European market remained firm despite weakness in some vegetable oil markets. June ARAG FAME traded around $1,525/mt while RME averaged $1,578/mt and UCOME averaged $1,691/mt. HVO Class II traded at a $1,320/mt premium and SAF changed hands at a $1,300/mt premium, implying flat prices near $2,821/mt for HVO and $2,921/mt for SAF. Physical activity remained healthy with UCOME changing hands between $580 and $625/mt premium and HVO trading at $1,320/mt premium. BOGO strengthened further to approximately +680 while BOPO held near a historically high spread of +587. The continued strength in soybean oil relative to gasoil confirms that the market is increasingly pricing policy support and feedstock scarcity rather than simply following petroleum markets.

The most important development remains D4 RINs. At nearly $2.38, RIN values have already reached levels that many refiners consider problematic. If inventories continue falling and policymakers maintain aggressive biomass-based diesel targets, a move toward $2.50 or higher cannot be dismissed. At those levels, independent refiners focused on maximizing crack margins would begin accumulating enormous compliance liabilities. This creates a genuine three-alarm fire for refiners without meaningful renewable fuel production. They face higher crude prices, tightening refined product inventories, and rapidly escalating RIN obligations simultaneously. The administration's challenge becomes increasingly clear. Maintaining ambitious renewable fuel targets supports soybean oil, biodiesel, and renewable diesel demand, but every increase in RIN values transfers additional costs into the petroleum supply chain. Monday's market action suggests traders increasingly believe inventory fundamentals matter more than peace headlines, and right now those fundamentals continue pointing toward tighter energy markets rather than looser ones. Fasten your seatbelts.

Comments