RINs Weak, Gasoil Cracks, and U.S. Trade Flows Under Fire

- Henri Bardon

- Sep 11, 2025

- 2 min read

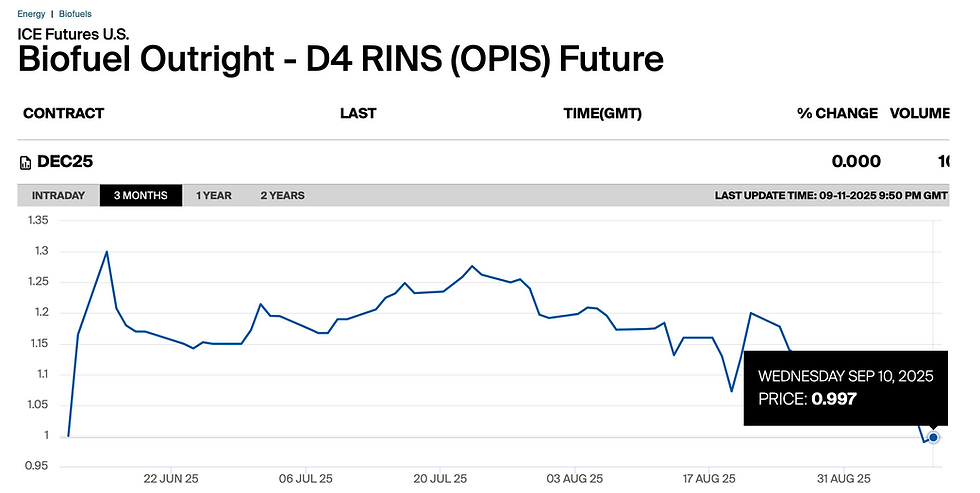

D4 RINs continue to trade under pressure, slipping below the $1 mark and leaving U.S. biodiesel economics firmly negative. The U.S. screen biodiesel crush margin remains about 55¢/gal in the red, worsening to nearly 60¢/gal negative when marking D4s at 95¢. With compliance support this weak, blending remains uneconomic, and U.S. producers are squeezed between high feedstock costs and soft credit values.

The sharp 2% drop in ICE gasoil was the defining move of the day. The fall was surprising given ongoing geopolitical tensions, and it may point less to fundamentals than to political fragility within Europe — particularly in France, where internal strains are spilling into markets. But the move could also be read as a signal: a market beginning to price in the possibility of sanction fatigue. Washington’s sudden decision to lift restrictions on Belaruss' Belavia and reopen direct flights to US from Minsk hints at a potential broader recalibration. If Russian sanctions were to ease, however unlikely it sounds currently amid the noise, the implications for energy flows and cracks would be quite profound and no trader should ignore this.

For Indonesia, POGO remains insulated by the $375/mt export levy, which bridges the gap and keeps flows viable. Yet the real risk lies not in the spread but in politics: the country faces internal unrest and budget battles, with riots largely concealed under a media blackout. This instability raises serious doubts about the sustainability of the levy mechanism, and by extension, Indonesia’s role as the anchor supplier of palm-based biodiesel.

In Europe, ARAG window activity showed steady participation but at lower levels than earlier in the week. FAME 0 cleared four times at $685/mt, pulling the flat price back to $1,363/mt. RME traded at $740–742/mt, implying a flat price of $1,418/mt, while UCOME moved at $794–795/mt for a flat of $1,473/mt. The RME/FAME spread held at +$55/mt, while UCOME/FAME widened to +$109/mt. Liquidity was healthy across grades, but the tone remained heavy as weaker gasoil weighed on biodiesel cracks. Germany has released statistics that show that trade in Biodiesel has slowed significantly in 2025 Vs 2024.

The most worrying development on the grain side was South Korea’s decision to buy corn in Brazil despite cheaper U.S. offers. Purina Korea booked 67,000 tons for November shipment at $245.41/t CFR, and MFIG secured another 63,000 tons for December arrival at $232.10/t CFR. These purchases underscore how importers are increasingly willing to pay more for Brazilian origin, widening the spread between Brazil and the Pacific Northwest and further eroding U.S. competitiveness in global trade in the face of a bumper crop in the U.S.

Looking forward, three events will dominate market sentiment over the next month: the U.S. government closure debate in Congress before Sep30, the October 14th Section 301 USTR review on China vessel tariffs, and the upcoming Golden Week (first week of October) holidays in China. Each carries the potential to disrupt flows and price relationships across energy, agriculture, and biofuels. Against that backdrop, today’s gasoil weakness may not just be about oversupply — it may be the market’s early tell that political currents are shifting faster than most expect.

Comments