RINs Ignore the Crude Selloff as Hormuz Refuses to Normalize

- Henri Bardon

- 23 hours ago

- 6 min read

Quick note before today’s market recap.

This Substack is now one year old. In that time, it has grown into a global daily comment read by traders and market participants across Singapore, Europe, the United States and South America. We are now close to 500 subscribers, and readership is up 91% over the past year.

The focus remains a trader’s point of view on biodiesel, renewable diesel, SAF, feedstocks, RINs, LCFS, freight, refinery margins and policy risk. The goal is to connect the screens, the physical market and the policy tape into a daily view of what is moving price.

Not all subscribers are paid. If you read this regularly and find it useful, please consider contributing at least $1 per day to my substack: https://substack.com/@henrijeanbardon It helps keep the work independent, consistent and focused on the global signals traders need to follow.

Monday’s tape looked easy at the crude level and tight everywhere else. WTI fell 38 cents to $68.31 and Brent fell 23 cents to $71.89, while Saudi Aramco cut August Arab Light OSPs into Asia by $11/bbl, from a $9.50/bbl premium for July to a $1.50/bbl discount for August. West African crude differentials stayed under pressure as extra Middle Eastern grades, U.S. WTI flows into Europe and SPR barrels competed for refinery demand. Crude looks supplied. Refined products do not. ICE Gasoil July rose $23/mt to $966.50, August rose $22/mt to $945.25, and Jul/Dec widened $8.75/mt to $145.50. Flat gasoil rose by about half a standard deviation, while the backwardation move was closer to a two-standard-deviation stress signal.

The product cracks are the clearest reason why the crude selloff did not translate into a bearish biodiesel/RD read. The U.S. 3:2:1 crack pushed to 61.57, a new high on our chart, while the heat crack stayed near 69.98. RBOB August gained 7.91 cents to 2.9964/gal and ULSD August gained 10.75 cents to 3.2897/gal. Physical diesel is now priced at a wide premium to crude across the U.S., with midday indications around $137.25/bbl on the Gulf Coast, $141.34/bbl in New York Harbor, $126.94/bbl in Group 3, $122/bbl in Chicago and $142.17/bbl in Los Angeles against WTI near $68.80. Refiners have every incentive to run, but product supply still looks tight. For biodiesel and RD, the replacement value of distillate remains high even as crude trades softer.

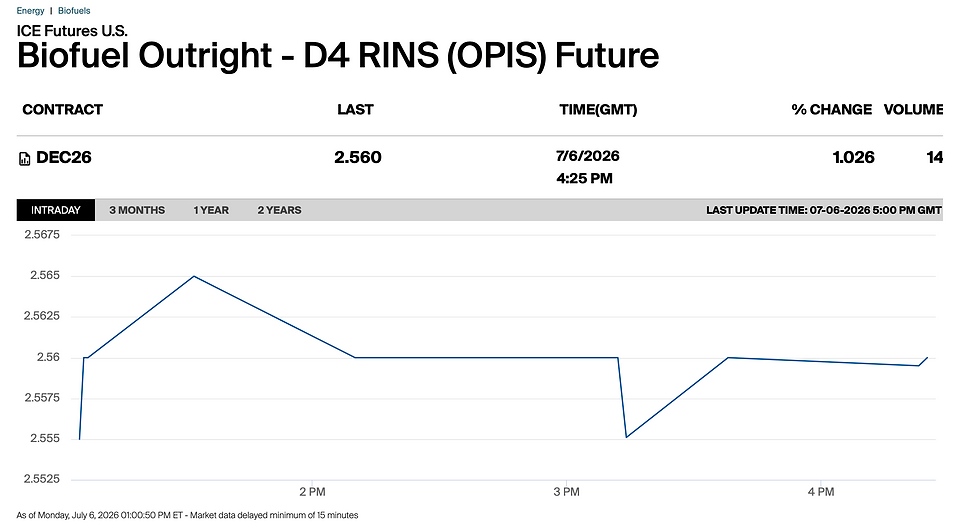

D4 RINs are still saying the U.S. needs more physical generation. Dec D4 RINs traded at 2.56, up 1.026%, with 14 lots on screen. The front U.S. biodiesel screen crush improved as heating oil outran bean oil, with the August RD crush up 3.33% to 1.0261/gal and the August conventional biodiesel crush up 3.01% to 1.4425/gal. The deferred crush was weaker, with Dec RD down 1.95% to 0.8734/gal and Dec conventional down 0.50% to 1.2826/gal. That split fits the market. Front product tightness helps blending economics, while deferred feedstock cost and RIN uncertainty still cap forward margins.

Bean oil was the large feedstock signal. July soybean oil rose 1.40 cents to 68.35 c/lb, up 2.09%, while September rose 0.92 cents to 67.26 c/lb. In $/mt terms, July bean oil moved to $1,506.84/mt, up $30.86, and September moved to $1,482.37/mt, up $19.84. BOPO made the cleaner relative-value move, with July BOPO up $30.86 to $399.84 and September BOPO up $20.28 to $360.81. That is roughly a two-standard-deviation move. Palm did not confirm the same stress. CPO screens were flat around $1,107-1,135/mt through Dec, while MPOA put June Malaysian production up 10.09% to roughly 1.67 mmt and market polls point to June palm stocks up 2-3% to 2.48-2.50 mmt. This was a U.S. bean oil and RFS repricing, not a palm-led rally.

The April U.S. feedstock mix supports the same conclusion. Soybean oil rose to 38% of biodiesel/RD feedstock use in April 2026 versus 32% in April 2025. Canola oil rose to 11% from 5%. Tallow fell to 20% from 29%, yellow grease fell to 14% from 17%, corn oil stayed at 15%, and white grease stayed near 2%. The U.S. is pulling more vegetable oil into compliance at the same time global palm supply looks less tight. This is the RFS island effect in numbers. U.S. policy is forcing local vegetable oil demand higher even while global vegoil spreads still argue for substitution.

China added another layer to the bean oil story. U.S. soybean export sales were only 1.5 mbu versus a trade estimate of 11-23.9 mbu, while new crop sales were 6.7 mbu. Old crop soybean sales still remain 18.3 mbu, or 1%, ahead of the required pace. China and Japan were the main old crop buyers, while Mexico led new crop. The market is also trading the possibility of stronger Chinese participation after tariff chatter improved sentiment. The Chinese buying base is low. The chart through late February showed 25/26 U.S. Gulf soybean cargoes to China at 7.9 mmt and PNW at 4.2 mmt, versus 17.8 mmt and 10.4 mmt in 24/25, and 19.0 mmt and 10.5 mmt in 23/24. Any sustained Chinese return would matter because RVO demand already keeps the domestic oil balance tight.

Hormuz remains the main reason not to accept the “back to normal” crude narrative. Reported vessel crossing data showed 34, 48 and 38 crossings over recent days versus a pre-war average of roughly 125-140 crossings per day. Reported Kpler estimates put June oil exiting the Strait near 5 mb/d on average, about one-quarter of the roughly 20 mb/d pre-war flow. The inbound tanker list also changed after July 3. July 3 showed 15 inbound tankers, July 4 showed 6, and July 5 showed only 4 so far, including Gas Warich, a sanctioned LPG tanker using the Oman lane. Reported satellite imagery dated July 6 also showed 40-45 IRGC speedboats operating in the Strait. This is not full normalization. It looks more like controlled movement, selective routing and a rush to move delayed cargo during a fragile window.

Fertilizer deserves attention in the same Hormuz context. Iran’s chemical exports are concentrated in methanol and urea, which represented almost 69% of its 2025 chemical export slate in the chart provided. Fertilizer flows through the Strait were weak for several weeks, then rebounded to roughly 608 kt and 680 kt in the late-June weekly data. That rebound should not be confused with a durable return to normal logistics. Insurance costs, vessel availability, threat levels and routing controls remain part of the freight equation. Nitrogen prices matter for corn and soybean acreage economics, and any renewed fertilizer disruption feeds back into crop cost structure.

The USTR Section 301 issue now belongs in the same logistics paragraph as Hormuz. The measure targets vessels and operators, not UCO, biodiesel or RD cargo directly, but the commercial impact hits freight. If a U.S.-bound shipment uses Chinese-owned, Chinese-operated or Chinese-built exposed tonnage, carriers have a strong incentive to pass costs through as freight, surcharges or altered service. With the October deadline approaching, importers have reason to land UCO, biodiesel and RD cargoes sooner, before vessel nomination, charter-party wording and carrier surcharges become harder to manage. Chinese retaliation risk adds another layer because vessel owners allocate fleets globally, not lane by lane. For U.S. biofuel imports, this is no longer a footnote. It is part of landed cost.

Europe confirmed a firm physical biodiesel tape. The AOM window printed 14 deals, with UCOME trading 615-635, RME 535-540, FAME 500, HVO Class I at 1160, HVO Class II at 1255-1260 and SAF at 1150. SunCo settlements put RME at $1,512/mt, up $9, FAME at $1,443/mt, up $18, UCOME at $1,585/mt, up $6.02, and HVO II at $2,693/mt, up $59.07. TFS showed Jul RME at 1463/1483, FAME 0 at 1423/1443, UCOME at 1573/1593 and HVO at 2628/2648 FOB ARA. July differentials were 515/535 for RME, 475/495 for FAME, 625/645 for UCOME and 1680/1700 for HVO. The paper market also shows July month-to-date averages of $1,489.54 for RME, $1,437.64 for FAME 0 and $1,588.37 for UCOME, with UCOME/FAME at $150.73 and RME/FAME at $51.90.

The trading message is clear. Crude is pricing extra barrels, lower Saudi OSPs and softer differentials. Biodiesel/RD is pricing product scarcity, compliance demand, higher bean oil, a tighter gasoil curve and freight risk. BOPO up 8.36%, gasoil Jul/Dec at $145.50/mt and D4 RINs at 2.56 are not bearish signals. They show a market where crude has relaxed, but the renewable diesel, biodiesel and compliance chain has not.

Comments