Diesel Market Flashing Red While Soybean Oil Stocks Finally Begin Drawing

- Henri Bardon

- 4 minutes ago

- 4 min read

Energy markets closed the week with increasing concern that the Middle East conflict is entering another phase rather than approaching resolution. Crude rallied sharply again with July Brent settling at $109.20/bbl and June WTI at $105.24/bbl. More importantly, the structure continues to tighten aggressively with WTI Jun/Dec widening to +$21.88/bbl and Brent Jun/Sep at +$8.84. ICE gasoil settled at $1,162.50/mt while Jun/Dec backwardation widened further to +$262.75/mt. Those are levels normally associated with acute prompt supply stress rather than a simple geopolitical headline premium.

Distillates and jet fuel again led the complex higher. European ULSD CIF cargoes jumped another $58.75/mt to $1,226.75/mt while Mediterranean cargoes traded near $1,241/mt. Singapore jet fuel rose back above $155/bbl while Fujairah jet reached $156.10/bbl. NWE jet cargoes surged more than $60/mt on the day toward $1,343/mt. SAF FOB NWE meanwhile traded above $3,040/mt. The market continues signaling that middle distillates remain the most vulnerable part of the barrel if Hormuz disruptions persist into next week.

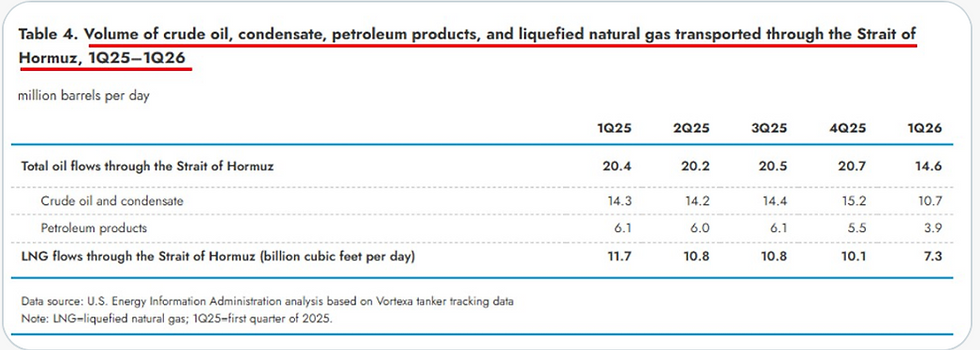

The physical backdrop also remains supportive. Preliminary shipping data discussed in the market today showed only 11 Hormuz crossings on Wednesday and 7 on Tuesday, confirming that flows remain heavily disrupted even if some Chinese-linked vessels are beginning to move again. At the same time, front-end diesel curves continue tightening globally with Singapore 10ppm gasoil near $162.73/bbl and Fujairah 10ppm above $158/bbl.

The interesting feature today was that feedstocks did not fully confirm the strength in diesel. NOPA April soybean crush came at 211.856 million bushels, below the average trade estimate of 214 million. Soyoil stocks printed 1.947 billion pounds versus expectations near 1.954 billion pounds. Inventories remain up 28% year-on-year, showing that soyoil availability is still comfortable, but the draw versus March confirms stocks are no longer building aggressively. This explains why soybean oil held relatively firm at 73.90 c/lb despite broad weakness across grains and disappointing China trade headlines.

The result was another sharp collapse in BOGO as diesel outran feedstocks. Jul BOGO fell to +$466.70/mt, down more than $44/mt on the day, while bean oil expressed as a percentage of gasoil dropped another 4% to 1.4006. BOHO also collapsed to 1.6212 despite heating oil futures settling near 3.9220/gal. The market is no longer relying on a bullish agricultural narrative to support biofuels. Instead, mineral diesel and jet fuel tightness are now pulling the entire renewable complex higher.

The ARAG market remains exceptionally strong despite some consolidation into the weekend. FAME 0 traded near $1,446/mt flat price while RME reached approximately $1,509/mt and UCOME above $1,638/mt. UCOME premiums against gasoil remain historically elevated near +$492/mt while RME premiums are still above +$360/mt. HVO Class 2 remains close to $3,000/mt outright with escalated values still above $1,740/m3. European paper activity was lighter into the weekend with Q3 RME trading around +381 and Jun FAME around +265, both well below prior settlement levels, suggesting some risk reduction rather than confidence that physical tightness is ending.

Margins across the renewable complex remain historically strong. Conventional biodiesel crush margins for nearby periods improved again toward $0.87/gal while RD-oriented crush economics climbed above $0.33/gal in your matrix. RME/RSO margins also remain healthy near $194/mt while UCOME/FAME spreads stayed above $140/mt. Those economics continue encouraging maximum renewable fuel production even as feedstock values rise.

The physical soybean oil market outside the United States continues to look substantially cheaper than domestic U.S. values. Brazilian soybean oil FOB Paranagua paper indications remain deeply discounted with nearby June offers near -2030 to -2100 points versus CBOT soybean oil. That continues reinforcing the “RFS island” effect where U.S. policy and renewable diesel demand keep domestic bean oil structurally elevated relative to global vegetable oil markets.

RINs continue confirming the strength underneath the renewable complex. D4 RINs held above $2.04/RIN with Dec26 trading around $2.05 despite softer soybean oil fundamentals. Renewable diesel California credits also remain elevated with RDCA trading near 3.4856. The market continues pricing strong compliance demand into the second half of the year.

Another important political development came from Iowa and Missouri filing suit against New York over its mandatory GHG reporting program for fuel suppliers. The lawsuit reflects increasing tension between agricultural states and state-level LCFS style programs that impose reporting and compliance burdens on out-of-state biofuel producers using GHG as metric. This battle likely becomes more important as more states attempt to introduce carbon-intensity based fuel systems.

China also remains an important wildcard. Markets were disappointed that the Trump-Xi discussions produced little immediate agricultural demand. News reporters made the interesting observation that the announced purchase of 200 Boeing aircraft by China represents a value roughly comparable to annual U.S. soybean exports to China. The implication is that China may currently prefer strategic industrial purchases over large near-term agricultural commitments.

Despite the still-comfortable soybean oil inventories, the broader message from the market remains increasingly clear. Feedstocks are available. Distillates are not. If Middle East tensions intensify further next week while inventories continue drawing, diesel and jet fuel prices appear positioned to move substantially higher, dragging biodiesel, renewable diesel and SAF along with them.

Comments